Supreme Court holds VAT Not Applicable to Reliance’s Supply of Gas from KG Basin to UP which is an Inter-State Sale

![]()

- Introduction

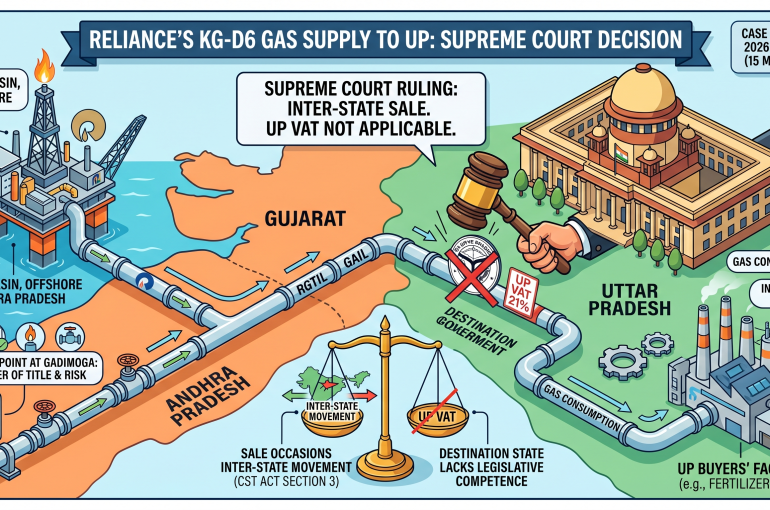

In State of Uttar Pradesh & Ors. v. Reliance Industries Limited & Ors., 2026 INSC 491, decided on 15 May 2026, the Hon’ble Supreme Court of India, comprising Justice J.K. Maheshwari and Justice Atul S. Chandurkar, clarified a crucial aspect of state taxation powers regarding the inter-State movement of natural gas under Section 3 of the Central Sales Tax (CST) Act. The Apex Court held that the supply of natural gas by Reliance from the KG-D6 basin in Andhra Pradesh to buyers in Uttar Pradesh constitutes an inter-State sale, ruling that the destination State lacks the legislative competence to levy Value Added Tax (VAT) on such transactions to prevent multiple taxation on a single movement of goods.

- Brief Facts

The factual matrix of the dispute centers on the extraction and sale of natural gas by RIL. RIL operates under a Production Sharing Contract (PSC) with the Government of India for the KG-D6 block located off the coast of Andhra Pradesh.

Pursuant to the Gas Sales and Purchase Agreement (GSPA) executed between RIL and various buyers in Uttar Pradesh, the designated “Delivery Point” for the natural gas is located at Gadimoga in Andhra Pradesh. At this point, the property (title) and the risk associated with the gas pass to the respective buyers. The gas is subsequently transported via an interconnected pipeline network, first through Reliance Gas Transportation Infrastructure Ltd. (RGTIL) to Hazira, Gujarat and then through the Gas Authority of India Limited (GAIL) pipeline to Auraiya, Uttar Pradesh, eventually reaching the buyers’ factories.

The Assessing Authority in Uttar Pradesh treated these transactions as intra-State sales and imposed a VAT at the rate of 21% on RIL. Aggrieved by the assessment, RIL challenged the order before the Allahabad High Court, which quashed the assessment, holding that the transaction was an inter-State sale. The State of U.P. subsequently appealed to the Supreme Court.

- Issue of Law

The primary legal issue before the Supreme Court was whether the sale of natural gas by RIL to purchasers located in Uttar Pradesh qualifies as an “intra-State sale” subject to the levy of U.P. VAT, or an “inter-State sale” governed by Section 3 of the Central Sales Tax (CST) Act.

A critical sub-issue hinged on the State of U.P.’s contention regarding the physical nature of natural gas. The State argued that because natural gas is a fungible commodity moving in a co-mingled form through a common carrier pipeline, it cannot be individually identified or appropriated to a specific purchaser until it is physically received at the buyer’s facility in Uttar Pradesh. Therefore, the State claimed the actual sale concluded within its borders.

- Analysis of Judgment

The Supreme Court undertook a rigorous examination of the contractual terms, specifically the GSPA, alongside the statutory framework of the CST Act. The core test under Section 3 of the CST Act for an inter-State sale is whether the contract of sale “occasions the movement of goods” from one State to another.

The Court observed that under the GSPA, the transfer of title and risk explicitly occurs at the Delivery Point in Gadimoga, Andhra Pradesh. The subsequent transportation of the gas through the pipeline network to Uttar Pradesh is an integral and inextricable incident of the contract of sale. The movement of the goods was a direct result of the covenant between the buyer and the seller.

Addressing the State of U.P.’s argument regarding the fungibility and appropriation of the gas, the Court found the reasoning legally untenable in the context of inter-state trade. The physical characteristics of the goods and the method of transport (co-mingled in a pipeline) do not alter the fundamental nature of the transaction. The Court firmly rejected the notion that the state could utilize such arguments to “override the constitutional scheme of legislative competence or to create taxing jurisdiction where the Constitution has not conferred any.” The Court explicitly stated that allowing the State of U.P. to levy VAT in this scenario would unlawfully enable multiple taxation on a single inter-State transaction, a field exclusively reserved for the Union.

- Conclusion

The Supreme Court dismissed the appeals filed by the State of Uttar Pradesh, upholding the well-reasoned judgment of the Allahabad High Court. This ruling provides crucial certainty for the energy sector and industries relying on inter-state pipeline networks. By strictly interpreting the incidence of sale and the movement of goods under the CST Act, the Court has safeguarded the constitutional guarantee against arbitrary and overlapping state taxation. The judgment stands as a robust precedent affirming that where a contract intrinsically necessitates the cross-border movement of goods, the transaction remains an inter-State sale, completely immune from localized VAT assessments at the destination.

ANIKET KUMAR PARCHA

Legal Associate

The Indian Lawyer & Allied Services

Please log onto our YouTube channel, The Indian Lawyer Legal Tips, to learn about

various aspects of the law. Our latest Video, titled “Defamation on Social Media: Can a Meme Become a Crime?”, can be viewed at the link below:

Leave a Reply